Reconciliation is an accounting process that compares two sets of records to check that figures are correct and in agreement. Companies use this process to prevent balance sheet errors on their financial accounts, check for fraud, and to reconcile the general ledger.

There is no standard way to perform an account reconciliation. However, generally, double-entry accounting is performed where a transaction is entered into the general ledger in two places. It is the most prevalent tool for reconciliation.

Another way of performing a reconciliation is via the account conversion method. Here, records such as receipts or cancelled checks are simply compared with the entries in the general ledger, in a manner like personal accounting reconciliations.

There are four main reasons that account balances don’t match the underlying documentation:

- Timing differences

The delay between the money leaving one account and reaching another one may be measured in minutes or hours, not days or weeks.

2. Fraud

Careful attention to detail and review of reconciliations by someone who doesn’t work with that account can help catch many instances of fraud.

3. Missing transactions

4. Mistakes

Transaction hit the wrong account, Excel spreadsheet you used to calculate the journal entry has a formula error, a bank error. Some or all of these will happen at some point in the life of every business.

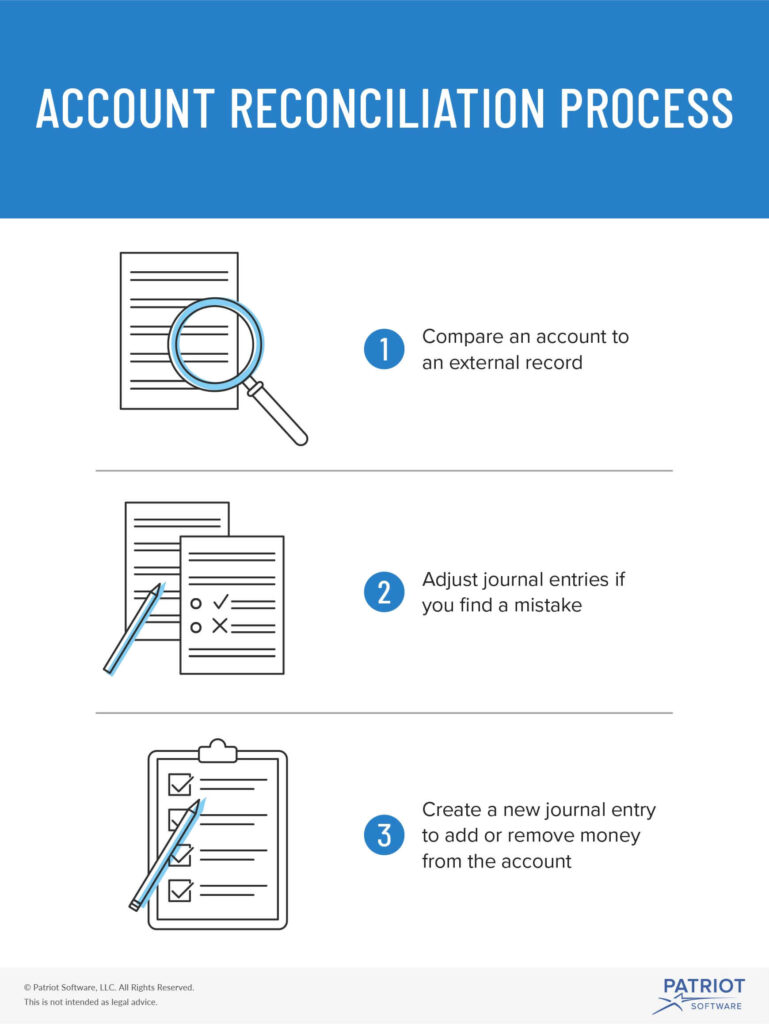

While there is no prerequisite for most businesses to reconcile regularly, doing so is a good habit as it will mean that business and financial information is up to date. Additionally, reconciling regularly is now made easy with a few simple steps:

- Access the internal source of data being reviewed and compare it against the external document it is being compared against.

- Make a note of the closing balance on the external document and compare its value to the closing balance of the corresponding account in your accounting software.

- Update the internal data source being reconciled to record all new transactions from the external document.

- Once all legitimate missing or duplicate transactions have been posted or removed, the closing balance on the account being reconciled should agree to the closing balance of the external document it is being reconciled against.

Reconciling accounts and comparing transactions helps your accountant produce reliable, accurate, and high-quality financial statements. Since your company balance sheet reflects all money spent, whether cash, credit, or loans, and all assets purchased with those funds, the accuracy of the balance sheet strongly depends on the accurate reconciliation of your company’s financial accounts telling us that the key role that reconciliation plays in making sure your numbers are right means that anyone who works with financials needs to master the reconciliation process.