GIFT City IFSC for Indian Businesses: Tax Benefits, Setup Process & What Every CFO Should Know

You are conducting cross-border transactions, paying full GST, full corporate tax and yet falling short on pricing due to your competitors who operate out of Singapore and Dubai. Indian CFOs are always under the pressure of improving their competitiveness in the global market despite the increase in compliance cost and taxes. But what if you had a legally recognized way of leveraging global financial advantages without relocating your firm?

The solution lies in the concept of GIFT City and its International Financial Services Centre (IFSC). Being India’s global financial center, GIFT City comes up with great tax advantages and flexibility along with simplified foreign business for qualifying firms. It’s increasingly becoming an operational base of Indian firms looking to operate on a global scale.

This article is your guide to the tax advantages, qualifying conditions, setting up and all that a CFO needs to consider before joining the GIFT City IFSC by 2026.

1. What makes GIFT City different from operating onshore ?

Most of the Indian enterprises see GIFT City as another SEZ. However, there are fundamental differences between GIFT City IFSC and onshore India. For instance, according to FEMA regulations, GIFT City IFSC is treated as foreign territory, which means that enterprises are able to operate in foreign currency, raise funds internationally, and serve international customers with greater flexibility compared to an onshore Indian company.

As for CFOs, they will notice significant changes in the operational process right away. First, while onshore enterprises have to operate mainly in INR and interact with several regulatory bodies (such as RBI, SEBI, IRDAI, and so on), depending on the type of activity, IFSC enterprises can use a unified regulation scheme under one regulatory body – IFSCA.

Another significant difference between the two is taxation and global positioning. For instance, while onshore enterprises operate with higher domestic tax liability and strict FEMA regulations, IFSC enterprises are eligible for numerous tax breaks and relaxed regulations for international transactions. Therefore, IFSC enterprises have an opportunity to compete with businesses from Singapore and Dubai on equal terms.

2. Tax benefits

The real draw of the GIFT City IFSC for most businesses is not about branding or location, but rather is purely tax-driven. This scheme allows India to compete at a global level in regard to cross-border transactions and services. The benefits provided in 2026 are strong enough to affect the bottom line of businesses, as well as the group structuring and treasury policies that they choose.

The most important provision concerns an updated Section 80LA. Under this scheme, all the income earned from certain activities in IFSC will be subject to a 100% income tax deduction for ten years out of 25 years. Due to this significant tax provision in the Budget 2026, the incentives provided by IFSC have become one of the best in India.

Moreover, a business working within a certain type of IFSC can enjoy a corporate tax rate of 15% instead of the usual 25–30%. The gap between these rates can significantly change the overall competitiveness of an entity against other off-shore jurisdictions such as Singapore or Dubai.

The benefit that arises out of GST is quite relevant, particularly in service-based companies. Services offered within the framework of the IFSC or even those offered to offshore customers may be eligible for zero GST rates, which will help save indirect taxes and improve cash flow within the system. This will be beneficial for industries such as fintech, consultancy, fund management, IT, aviation leasing, and global capabilities centers.

There are some valuable transaction-related exemptions offered by the IFSC platform. Firstly, there are no Securities Transactions Tax and Commodities Transactions Tax levied on IFSC transactions. Many financial transactions undertaken within the framework of the IFSC model are also not liable for stamp duty charges.

One of the greatest advantages of using the IFSC platform is the operational flexibility in foreign currencies. In contrast to regular Indian enterprises where there are restrictions on foreign currency, the IFSC platforms do not need mandatory INR conversion and are subject to lower FEMA constraints.

Nevertheless, a time aspect that needs careful attention is required by CFOs. Most of these incentives need the companies that are entitled to them to be in operation by March 2030. With an increase in the number of companies joining the sector and growth in regulation, those companies that move first will probably have the greatest structural benefit.

The tax structuring for a business within the GIFT City IFSC can be done in a manner such that the business receives optimal benefits under Section 80 LA while remaining aligned with regulations. This is achieved by the direct tax team at RNM.

3. Does your business qualify? Eligibility explained simply

Although the tax breaks provided in GIFT City IFSC are tempting, they may not apply to all businesses. The scheme has been created with cross-border financial services in mind, and its success will greatly depend on how you organize and incorporate your firm. There are several questions that CFOs need to answer before proceeding further.

- Is your business engaged in an eligible IFSC activity?

Some of the most popular activities include International Banking Units (IBUs), alternative investment funds (AIFs), insurance and reinsurance companies, fintech organizations, aircraft leasing companies, global treasury centers, and corporate treasuries of multinational corporations.

- Is this a genuine creation of a new IFSC unit?

This point is critical, since if authorities conclude that your project does not create anything truly new, you will not be able to enjoy tax breaks provided by Section 80LA.

- Will you get the mandatory approvals from the regulators?

An eligible business entity needs to obtain registrations/ licenses according to the governing structure of International Financial Services Centres Authority (IFSCA), as well as any related banking/insurance/ securities legislation based on the type of transaction.

- Are you ready to show that you are engaging in genuine IFSC transactions?

The business entity is required to have sufficient operational substance and compliance documentation as per the IFSC structure.

- Are you ready for annual compliance?

For continued tax benefits, the entity is expected to file the prescribed accountant’s report along with its tax return annually. Failure to comply may risk the tax benefits, even post-approval.

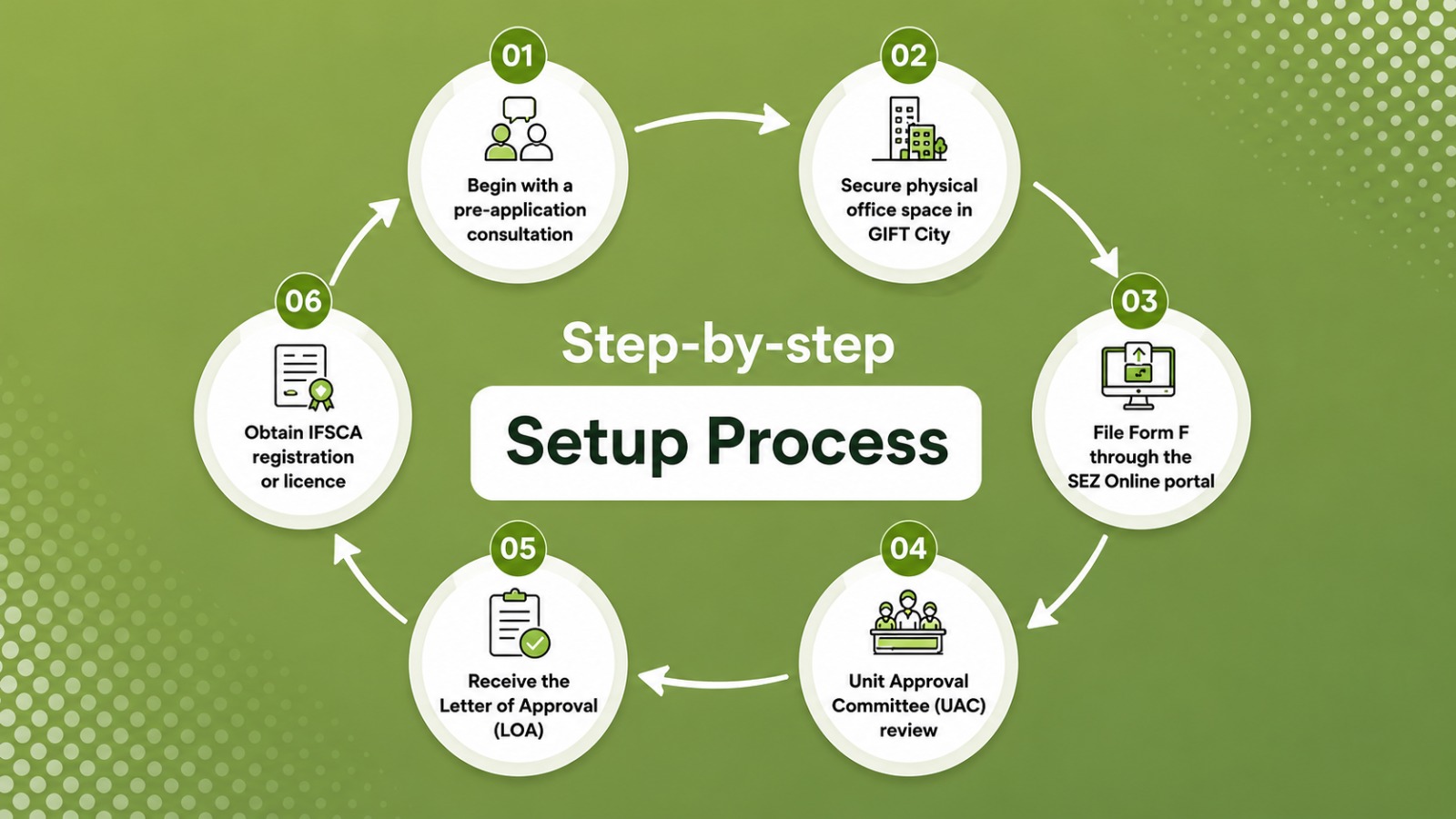

4. Step-by-step setup process

For many CFOs, the biggest hesitation around GIFT City IFSC is not taxation it’s uncertainty around the setup process. The good news is that the framework is far more structured and streamlined than most businesses expect. If the documentation and sequencing are handled correctly, a well-prepared application can move relatively efficiently.

Step 1: Begin with a pre-application consultation

Before incorporating anything, businesses should engage with the Development Division of International Financial Services Centres Authority (IFSCA). This early-stage discussion helps determine whether the proposed activity qualifies under IFSC regulations and clarifies the correct regulatory classification. This step is particularly important for fintech, treasury, and hybrid financial service models.

Step 2: Secure physical office space in GIFT City

A physical presence is mandatory. Virtual offices or purely registered-address structures are generally not sufficient for IFSC approval. Businesses must obtain office space within the IFSC zone and secure a Provisional Letter of Allotment (PLOA) from the SEZ developer. This becomes a foundational document for subsequent approvals.

Step 3: File Form F through the SEZ Online portal

Once the office allotment is secured, the applicant files Form F through the SEZ Online system to the Development Commissioner. This application outlines the proposed business activity, ownership structure, operational model, and projected international business operations.

Step 4: Unit Approval Committee (UAC) review

The application is then reviewed by the Unit Approval Committee (UAC), which typically meets weekly in hybrid mode. The committee evaluates regulatory fit, operational intent, and compliance readiness. Well-prepared applications with complete documentation generally move significantly faster.

Step 5: Receive the Letter of Approval (LOA)

Once approved, the entity receives the official Letter of Approval (LOA) under the SEZ Rules, 2006. This formally authorises the establishment of the IFSC unit and is a critical milestone in the process.

Step 6: Obtain IFSCA registration or licence

After receiving the LOA, businesses proceed with the final IFSCA registration or licensing process based on their activity category. For properly prepared applications, this stage generally takes around 4 to 8 weeks.

One critical point many businesses miss: the LOA must be secured before applying for IFSCA registration. Getting the sequence wrong can delay approvals, increase compliance costs, and trigger avoidable re-filings. RNM’s regulatory advisory team helps businesses manage the entire process from entity structuring and documentation to regulatory coordination and final registration.

5. What Budget 2026 changed – and why the timing is critical ?

GIFT City IFSC had been regarded by many CFOs over the years as an area of potential but was considered to be one which was in its formative stages. However, Budget 2026 has made significant alterations in terms of making long-term tax planning a much easier, more predictable, and financially appealing proposition.

Perhaps the most significant alteration involved increasing the period within which firms can utilize the Section 80LA provision from 15 to 25 years. Companies are now free to select any ten years within this increased period to enjoy 100% tax deduction on their income during that time period. In addition to providing more certainty, this has enhanced strategic maneuverability, allowing firms to take advantage of this provision during periods when they see the most financial success.

Additionally, budget 2026 has provided clear direction regarding the concessional tax status of firms in terms of treasury centers and cross-border operations.

But time is still ticking. Businesses which qualify need to start operations before March 2030 in order to be able to benefit from most of these advantages. Companies that make early moves will have enough time to optimise their systems.

That is why many companies are considering GIFT City at the moment – when everything is still possible and the regulatory situation is very friendly.

6. 5 mistakes Indian businesses make when setting up in GIFT City

The opportunities in GIFT City IFSC are significant, but so are the risks of getting the structure wrong. Many businesses lose valuable tax benefits not because the model is invalid, but because critical regulatory and compliance details are overlooked during setup.

Mistake 1: Restructuring an existing Indian business into IFSC

This is one of the most common errors. Businesses sometimes attempt to shift an existing domestic operation into GIFT City to access the Section 80LA tax holiday. However, if the IFSC unit is viewed as a split, reconstruction, or reorganisation of an existing Indian business, the tax deduction may be denied entirely.

Mistake 2: Applying to IFSCA before securing the LOA

The process sequence matters. Many companies approach International Financial Services Centres Authority (IFSCA) directly without first obtaining the Letter of Approval (LOA) under SEZ regulations. This often leads to delays, re-filings, or outright rejection.

Mistake 3: Missing the accountant’s report with the ITR

Even eligible businesses can lose the Section 80LA deduction for a financial year if the required accountant’s report is not filed alongside the income tax return.

Mistake 4: Choosing the wrong 10-year deduction window

The tax holiday is flexible, but poor timing can waste it. Some businesses start claiming deductions during low-profit years instead of aligning the benefit with peak profitability periods.

Mistake 5: Assuming GST exemption applies automatically

GST relief in IFSC is highly beneficial, but not universal. Exemptions apply only to specified transactions and qualifying services — not every activity conducted within GIFT City. Proper transaction structuring is essential.

Now that Budget 2026 has made its amendments, GIFT City IFSC has transitioned from a niche play to a strategic option for Indian companies with global aspirations. With the extension of the timeline for using Section 80LA and clarification on the tax structure, we can say there is now an opportunity available before March 2030 to optimize taxation and treasury.

Should your business be considering a move to GIFT City, how you decide to structure your operations will affect the amount of tax benefit you can reap. The experts from RNM have extensive experience advising Indian companies on IFSC-related matters.

Book a Consultation Now!

FAQ

1. Can an Indian company set up a subsidiary in GIFT City IFSC?

Yes. Indian companies can establish subsidiaries or units in GIFT City IFSC, provided the proposed activity falls under eligible international financial or cross-border business categories approved by the regulatory framework.

2. Is physical office space mandatory in GIFT City?

Yes. Businesses must maintain a genuine physical presence within the IFSC zone. Virtual offices or purely paper-based registrations are generally not sufficient for approval. A Provisional Letter of Allotment from the SEZ developer is typically required before registration.

3. How long does IFSC registration take in 2026?

For well-prepared applications with complete documentation, the registration and approval process generally takes around 4 to 8 weeks. Timelines may vary depending on the business activity and regulatory category.

4. What is the difference between DTA and SEZ in GIFT City?

The Domestic Tariff Area (DTA) follows standard Indian tax and regulatory rules, while the Special Economic Zone (SEZ) and IFSC areas operate under specialised frameworks offering foreign currency operations, tax incentives, and liberalised cross-border regulations.

5. Which businesses are not eligible for GIFT City IFSC?

Purely domestic businesses without international financial activity, entities created through reconstruction of existing Indian businesses, and operations outside approved IFSC sectors generally do not qualify for key IFSC tax benefits.